Allen Alley: PERS (Part I) - the Liability

Asking for a friend, do you have $8.7 billion to spare in 2043? That's the forecasted size of the State's PERS liability.

Technology entrepreneur and investor working to create opportunities for the next generation. Former Oregon GOP Chairman and candidate for Governor and Treasurer. Aspire to be a voice for those not heard.

Note from the author

This is the first in a two-part series of articles that examines the Oregon Public Employee Retirement System (PERS), the System’s liability, and the assets we have to protect PERS.

The PERS issue has two fundamental sides: the liability (how much money we owe) and the assets (how much money we have). One of the biggest issues we have when discussing PERS is that people comingle these factors. They interchangeably discuss the liability and the assets. The result is a huge amount of confusion. I will discuss the sides separately in two articles. The first focuses on the PERS liability and the second on the assets we have to meet that liability and other potential solutions.

Understanding the PERS liability

PERS is predominantly what is called a “defined benefit” pension plan. That means government employees are made promises to receive future monthly retirement payments, for life, based on their salary and length of employment. The biggest issue is the government needs to, but is not required to, fund a reserve that can fulfill the promise of future benefits.

In Oregon, like in many other states, we are not keeping pace with our funding. While the federal government can print money to offset liabilities, states can’t. We have to meet our liabilities with higher taxes, fees and fines or borrow money on the open market by issuing bonds. There is no magic printing press for us.

Think of it this way. You have a child and you promise to save enough for their college education. Your intent is to store away money each year for this inevitable payment. However, you find that as the years pass things come up — life happens. Maybe it is a new car or a vacation or a boat or a new house. You expect that your income will go up and maybe it does, but gosh it is hard to keep putting money aside for something that isn’t going to happen for 18 years. Then, suddenly, you realize your child is 15 years old and entering high school. You only have four years left and haven’t saved nearly what you needed to save.

"1994 - Carolyn's high-school Graduation - Woodbridge Senior High School Diploma 0168" by Claire CJS is licensed under CC BY-NC-SA 2.0

That is where Oregon is right now. The State has a figurative high schooler named PERS asking for lots of money in a short time. And, unfortunately, the State doesn’t know where to find it.

Over the years, we knew we should be saving, but golly that is hard to do when there are so many attractive things that are politically more glamorous and will pay higher electoral dividends than saving money for a retirement plan. We, thankfully, have saved something, but the cost of the promise we made years ago has grown faster and larger than we ever thought.

The size of the (growing) problem

There have been some attempts to control the liability. For example, there’s been some work to change the specifics of the plans for retirees. Some say that these modifications to PERS between Tier 1, Tier 2 and Tier 3 of the Oregon Public Service Retirement Plan (OPSRP) have largely eliminated the liability issue but that isn’t at all true. OPSRP has a defined benefit that is only about 10% less than that of Tiers 1 & 2. If OPSRP had eliminated the issue of an underfunded future promise, the PERS liability wouldn’t keep growing. Instead, it would tail off as people retire and ultimately pass away.

The PERS liability is well-defined and documented by the actuary the state hires to define the size of the liability is and how it changes over time. The actuary, Milliman, does an excellent job of consistently analyzing and forecasting the liability. Without their work, tracking it and understanding it would be impossible.

To calculate the PERS liability, Milliman needs to take into account the number of government employees, their current salaries, the projection of salary increases over the next 30 years and even their life expectancy (and the life expectancy of their spouses). These factors determine how much money should be set aside this year to adequately fund each employee’s retirement. Doing this calculation for the more than 375,000 people covered by PERS is a massive undertaking and thankfully Milliman does it well.

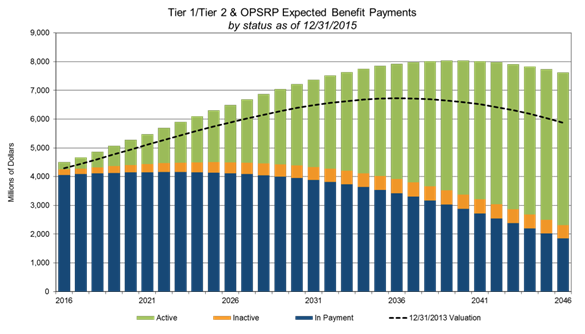

The graph above conveys the heart of Milliman’s work. It shows the cash payments government employers must make to retirees. These are the actual checks that are required to be written to retirees each year for the next 30 years. You will note that they start at about $5.4 billion in 2020 and rise to a peak of $8.7 billion in 2043 before tailing off to $8.3 billion in 2050.

The size of these numbers is hard to comprehend. To put things in perspective, the annual payroll of the currently active government employees (state, county, city, school district…) is about $11 billion a year. What that means is our payments to retirees this year of a little more than $5 billion is about 45% of the active payroll. Could you run your business if, for every dollar you pay your current employees, you had to pay $0.45 to people who no longer work for you?

The numbers make clear - the liability can’t be wished away

Some have pointed to this graph to say, “See there really isn’t an issue. All we need to do is get to 2043 and after that the payments trail off.” That may be the single most erroneous interpretation of this graph. As Milliman clearly points out every time they present this graph, “The graph does not include expected benefit payments for members hired after the valuation date.” What that means is this graph assumes there are never any government employees hired after the valuation date (in this case 12/31/2019). No new teachers, state employees, police or fire. No new county employees or city employees. No new hires at all. If you added in new hires (assuming the government hires at the same rate they have in recent history), the chart would not reach a maximum and then tail off. It would continue to grow, and grow, and grow.

The assumption that there are no new hires might sound unreasonable, but if you think about it, this chart reflects the out-of-pocket cash payments to the known State employees. The total cash-out-of-pocket over the next 30 years is about $238 billion (add up each of the bars representing payments for the next 30 years). The total cash-out-of-pocket for the life of all of the existing employees and retirees is obviously much more than that. The employees don’t all die in 2050 but, for the purpose of calculating the actuarial liability, Milliman cut things off at 30 years.

Just how much saving was (and is) required

"Stethoscope and piggy Bank" by 401(K) 2013 is licensed under CC BY-SA 2.0

Now that we understand the total cash liability the question turns to how much money should we have saved to cover that liability? This is the “actuarial liability” and that is what Milliman calculates based on current salaries, projected salary increases and life expectancy of the employees and their spouses. In order to do this, they need to pick an assumed rate of return. The assumed rate of return is how much investment income we think the State Treasurer can make on the money we set aside for these payments. If we assume we just stick the money in a virtual mattress, and get no return on investment, we need $238 billion. If we did that, the money would be safe, but not generating any investment returns. That’s why the State actively looks for investment opportunities.

Based off of those opportunities, the PERS Board approves an “assumed rate of return” and that is what Milliman uses along with the other salary and life expectancy data to determine the actuarial liability. The current assumed rate of return is 7.2%. That means the OIC believes, on average, the State will generate 7.2% return per year on the funds managed by the State Treasurer. Many of us would be thrilled to achieve an annual rate of return of 7.2% and we are fortunate that that is about what the track record for the Treasury has been in the past.

When Milliman does their calculation, they come up with an actuarial liability of $89.5 billion. This is the amount of money that if we had it invested at 7.2% interest we could cover the PERS liability for the existing employees. Then each year, all we would need to do is come up with the money required to support the retirement promises made to new hires.

What if the assumed rate of return was 5%? The actuarial liability would rise because you would need more cash now in your investments to cover the future payments. And, like I said before, if you put the money in the mattress and earned 0%, the actuarial liability would be $238 billion.

Why the numbers keep growing

When Milliman performs this analysis and calculation again in two years it will go up. Why? Because the governments (state, county, city, school districts) are hiring more people every year and those new hires are not included in the current forecast. So, even if we get to the point where we have enough saved to cover the existing employees, we need to add more for the new hires. How much more? Read on.

You can see the effect of the new hires if you go back and look at the same Milliman graph from 2015, merely four years ago.

Only four years ago, the total cash-out-of-pocket over the next 30 years was $213 billion. Milliman did their calculation of the actuarial liability and the result was $76.2 billion. What’s the upshot? In four short years, largely because of new hires, all of whom are in OPSRP (Tier 3), the cash-out-of-pocket liability increased by $25 billion or $6.25 billion per year and the actuarial liability increased by $13.3 billion or $3.3 billion a year.

To put these numbers in perspective, the new Corporate Activity Tax (CAT) passed by the legislature is expected to raise about $1 billion per year. Oregon government entities would need three brand-new CAT taxes, on top of the existing CAT, enacted every year just to keep up with the increases in the PERS liability. The PERS liability is HUGE and is rapidly increasing as government continues to hire employees.

A difficult, but necessary conversation

The reason this discussion is so important and why it is important to have outside of electoral politics is: do you think any politician could get elected if they came clean and said, “We have created a retirement system that is an iron-clad contract upheld by the Oregon Supreme Court that will pay $238 billion to retirees in guaranteed payments over the next 30 years. To fully fund this liability, we believe if we had about $90 billion in the bank, and if we could get a 7.2% return on investment, every year, for thirty years that we could cover the liability. Each year, this liability will grow around $6.25 billion and we believe if we could just save an additional $3.3 billion a year, we should be able to cover it. Please vote for me.”

"Oregon Elephant" by lightsoutfilms is licensed under CC BY-NC-SA 2.0

So there you have it. There’s an elephant in the room, but we seem to be too focused on our Zoom calls to see it. The elephant is a liability owed to more than 350,000 Oregonians that dwarfs any other State liability, yet we hardly discuss it. What makes this elephant even harder to dismiss is a contract with the 350,000+ members, as defined by the State Supreme Court, that must be upheld.

Our unwillingness to talk about PERS is not surprising. It’s not a fun topic to discuss. Even the largest tax hikes in Oregon’s history are only speed bumps that hardly have any effect on this rapidly growing liability.

The next installment will be an analysis of the resources we have to offset the liability and some ideas about how we can begin to expand the scope of the discussion to live up to our commitment to the PERS retirees, while maintaining the financial solvency of the State.

*******************

Keep the conversation going on our Facebook page: https://www.facebook.com/oregonway or via Twitter: @the_oregon_way