Allen Alley: PERS (Part II) - the Assets

When is $60 billion not enough? When you owe $238 billion…

Technology entrepreneur and investor working to create opportunities for the next generation. Former Oregon GOP Chairman and candidate for Governor and Treasurer. Aspire to be a voice for those not heard. @allen_alley

**Note from the author**

This is the second in a three-part series of articles that examines the Oregon Public Employee Retirement System (PERS), the System’s liabilities (Part I), the assets (Part II) and potential actions we can take to protect PERS and the retirees who count on it remaining solvent (Part III).

The PERS issue has three fundamental factors: the liability (how much money we owe), the assets (how much money we have), and the potential solutions (how we return to financial stability). One of the biggest issues we have when discussing PERS is that people comingle these factors. They interchangeably discuss the liability and the assets. The result is a huge amount of confusion. I am discussing the factors in separate articles to avoid that confusion.

Part III will run next Monday—December 21st.

The PERS liability review

PERS is largely a defined benefit plan. That means government employers make promises to employees that in the future, after they retire, they will be paid a percentage of their salaries for the rest of their lives and, in many cases, the lives of their spouses as well. The “benefit”— how much will be paid—is defined, but the “contribution” to fund that benefit isn’t quite as rigorously delineated.

The rules for defining how much money needs to be set aside allow for leeway and are interpreted and modified frequently. They remind me of the dialog from the movie “Pirates of the Caribbean,” when Captain Barbossa was explaining how and when the “rules” of the pirate’s code apply. “You must be a pirate for the pirate's code to apply and you're not,” the Captain clarified. He goes on to say, “The code is more what you'd call ‘guidelines’ than actual rules. Welcome aboard the Black Pearl, Miss Turner.”

Welcome, my friends, aboard the SS PERS. You are in for quite an adventure.

You see with PERS—the government employers don't always have to put aside enough money to meet the obligations of the promise. That is how we accrue an unfunded liability. The bottom line is the State of Oregon has an obligation to pay current employees and existing retirees $238 billion over the next 30 years.

The questions now are:

How much money do we have saved to cover those liabilities; and

How much more do we need?

Understanding the PERS assets

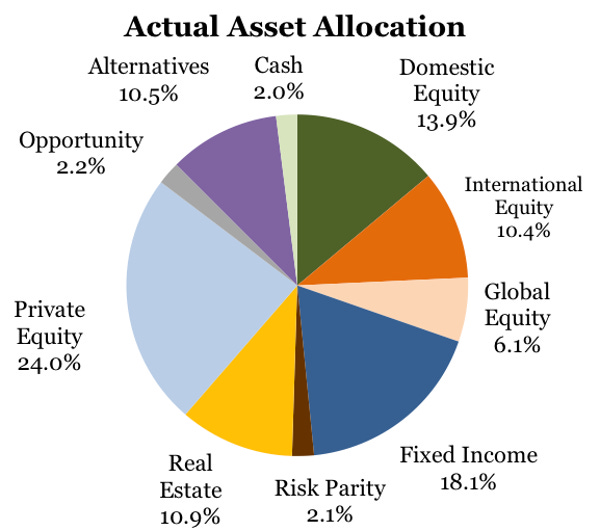

At the end of 2019, Oregon had about $60 billion in assets in the Oregon Public Employees Retirement Fund (OPERF) for defined benefit pension liabilities. These assets are managed by the Oregon State Treasury and are invested in a wide variety of publicly traded stocks, private investment (venture firms, private equity firms), real estate, fixed income (bonds), and other alternative investments.

In addition to the $60 billion that has been set aside, some government employers have borrowed money to make lump sum payments to offset their pension obligations. These payments are called “side accounts.” When they do this, they are counting on the Oregon State Treasury earning more on their borrowed funds than the interest payments they’ll need to make.

It is like taking a home equity line on your house to purchase stocks and bonds. If the income from your investment in stocks and bonds exceeds the increase in your mortgage payment, you are in great shape. But if the value of the stocks and bonds drops, you could be worse off than when you started.

These side accounts totaled about $5.3 billion at the end of 2019 and are invested alongside the other funds managed by the Treasury.

You may have heard account balance numbers that are higher than $65.3 billion ($60b in assets + $5.3b in side accounts), but that is because there is another level of confusion. (PERS is like an onion – the more we learn, the more we need to peel back additional layers). Beyond the funds that are directly tied to the pension liability, OPERF also manages about $12 billion in other retirement related funds. People often confuse these funds and talk about all of the Treasury funds being available to pay the pension liability. They aren’t. Only the $65.3 billion (and remember $5.3 billion of that is borrowed) is what we have saved against the $238 billion cash payouts required over the next 30 years.

How does Oregon make up the difference?

We need to earn income on the $65.3 billion.

How quickly we earn that income depends on a lot of factors: the stock market needs to do (very) well; real estate values need to (continuously) climb; renters need to make their rent payments; and, venture capitalists and private equity investors need to make great investments and generate (extraordinary) returns. Only if these investments generate their anticipated returns will the Treasury be able to beat out the interest owed on the side accounts and chip away at the wide gap between our assets and liabilities.

As an aside…this whole situation is a bit ironic. To pay the employee pension promises that were made but underfunded by various State entities we are now turning to Wall Street to provide extraordinary returns to bail them out.

How much do we need?

If you remember from the first article on the PERS actuarial pension liability, it is growing by about $3.3 billion a year. That is the amount that we should be setting aside to cover the pension promises made to new hires every year. We also need about $5.5 billion every year just to write checks to the people who have already retired and are currently collecting benefits. This will rise to $7.5 billion in just ten years and it continues to rise after that.

Quick math reveals our financial needs. If we take the total amount we need to fund our promise to new employees ($3.3 billion) plus the amount we pay retirees ($5.5 billion), we need $8.8 billion in cash. This defines our liability we need to cover next year.

What about the assets?

Let’s do a quick back of the envelope calculation of how much new money we need to come up with to cover the liability next year.

If we have $65.3 billion—and we make our targeted return of 7.2%—that gives us $4.7 billion. We should note that the 7.2% per year is a great return and might seem to be optimistic, but it is about the average return that the Oregon Treasury has delivered.

Now, is that enough?

No.

If we generate $4.7 billion from the investments and we need $8.8 billion, there's still a $4.1 billion gap.

Where will the funds to cover that $4.1 billion gap come from? The State has to borrow it, sell assets, or take it from you—the Oregon taxpayers—in the form of higher taxes, fees, and fines. After all, as you know, money doesn’t grow on trees. (Well, it sort of does in Oregon if we harvest them, but there are not enough trees, even in Oregon to come up with $4.1 billion).

Similarly, we can’t just “print” our way out of this. If the Federal Government runs out of money, they can either issue Government Bonds and borrow the money, or just print it. Local and state governments can borrow money and they do, but they don’t have the flexibility to print it. It has to come from taxpayers and citizens.

What does that estimated $4.1 billion hole mean for the State?

Does this mean the state will go bankrupt in 2021?

No, it doesn’t and it won’t. Aside from the fact that the ability for a state government to declare bankruptcy is debatable, Oregon won’t go bankrupt in 2021. Our legislature will raise some taxes, borrow some money, shift spending priorities, and continue to underfund the pension liability for another year. They will kick the proverbial can further down the road.

You may ask, “How long can this continue?”

There’s no specific timeline, but likely until the bond ratings get so bad that interest rates on the bonds exceed what we can get by investing the money in OPERF. Then, we will start blowing through the $65.3 billion reserve, dramatically cutting other state budgets and services or raising taxes, fees, and fines.

If we need to significantly tap the $65.5 billion in reserves that will create a whole other issue because about 40% of it is in very illiquid assets. That means they are assets that cannot be easily sold and if they were forced to sell, it would have to be done at a very deep discount to the value that we believe they are currently worth.

By way of comparison, assets like stocks and bonds can be traded relatively easily and are, therefore, “liquid.” You might not like the price, but you can sell them to quickly generate cash.

Investments in private equity funds, venture capital, and real estate funds are not easily traded and, therefore, are “illiquid.” Money in these illiquid investments can be locked up for ten years or more and if you were forced to sell your position, it would be at an extremely deep discount, if you’re permitted to sell at all.

There’s another layer we have to address: the cash flow within the portfolio. As mentioned above, it isn’t like all $65.3 billion is sitting in a bank and can be tapped at any time. About 40% of the portfolio is tied up in illiquid private funds. Cash requirements for these investments and investment returns (distributions) tend to be lumpy. For example, when the state agrees to invest $100 million in a private venture fund, that capital will not be invested up front but will be “called down” over several years. The capital also won’t instantly be returned. It may take 10 years or even longer to return the original $100 million and the profit. This means forecasting cash for these investments is difficult and, with 40% of the entire retirement portfolio invested in these funds, it makes cash flow management a big issue.

I don’t want to leave you the impression the Treasury or the oversight board—the Oregon Investment Council (OIC)—don’t understand these issues. They clearly do and take steps to discuss, vet, and implement alternatives. The problem is these issues are part of running a diverse portfolio of investments and they are exacerbated by fundamentally not having enough assets to cover the liabilities. At some point, a hole is just too large to fill. The Treasury and the OIC are forced to try to extract every bit of potential gain to make up for the chronic underfunding of the pension promises. The performance of the Treasury and the OIC has been good, but they are in an untenable position of providing cash to pay liabilities from an insufficient allocation of assets.

From what I have observed, it does not appear that any of the political types will do much to alleviate this situation. The only chance of them potentially taking action will be when retiree checks start to bounce. And, at that point, it is too late. This is one reason for these articles. I want to broaden awareness in the community of these issues and to encourage constituents to ask their elected representatives to take on this problem. There are several people who could raise this issue and begin to have a discussion about solutions. It starts with the Governor and the Treasurer. The Secretary of State could also play a role by using their audit authority to raise the issue. Alternatively, someone in the State Legislature could lead the effort.

Admittedly, though, I am not optimistic about any of these officials taking on this task. Officials who have attempted to take on PERS have borne tremendous electoral costs in the form of well-funded primary opponents. It makes perfect sense when elected officials see their colleagues vaporized in a primary for even the slightest attempt to address the PERS liability, that one would be reticent to even mention it.

PERS has replaced “sales tax” as the third rail of Oregon politics. Don't believe me? We now have a corporate sales tax and an automobile sales tax. We don’t have meaningful PERS reform.

**************************************************

Send feedback to Allen:

@allen_alley

Keep the conversation going:

Facebook (facebook.com/oregonway), Twitter (@the_oregon_way)

Check out our podcast:

#88